BIR Issuances – RMO No. 15-2025

The Policies and Procedures on Recording of Collections, Tax Receivables and Acquired Assets in Compliance with Reportorial Requirements of the Commission on Audit – Government Accounting Standards

Revenue Memorandum Order No. 15-2025

24 February 2025

Date of posting (BIR website): 20 March 2025

I. GENERAL OBJECTIVE:

This Order is hereby issued to:

- Amend Item III J of Revenue Memorandum Order (RMO) No. 36-2016, which states that in meritorious cases, a tentative financial report shall be submitted to concerned offices containing initially completed, validated and/or reconciled collection data.

- Provide additional procedures to RMO No. 13-2022 on recording of collection transfer between the national and regional office collection books to ensure completeness and accuracy of balances of the Cash-Treasury/Agency Deposit, Regular (CTADR) account.

- Reiterate guidelines on recording of Tax Remittance Advice (TRA) and Special Allotment and Release Order (SARO) in accordance with Section 62 of the Government Accounting Manual (GAM).

- Prescribe procedures to ensure proper disclosure of pertinent information on Tax Receivables in the Notes to Financial Statements (FS) in accordance with International Public Sector Accounting Standard (IPSAS) 19: Contingent Liabilities and Assets.

- Prescribe policies on disclosure of pertinent information on Acquired Assets in the Notes to FS in compliance with reportorial requirements of the Commission on Audit (COA).

II. GENERAL POLICIES:

1. The monthly, quarterly and annual consolidated Trial Balances (TBS), FS, and Supporting Schedules (SS) of the Bureau of Internal Revenue’s (BIR’s) National Government Collection Books (NGCB) shall be submitted to COA on the tenth (10th) day from the end of each month and quarter, and on/before January 31 (for the Revenue Regions) and February 14 (for the National Office) of the following year as prescribed under Chapter 19 Section 60.b and 60.c of GAM.

2. A monthly interim trial balance shall be generated thru the Electronic New Government Accounting System (eNGAS) by the Regional Finance Division (RFD) and Revenue Accounting Division — Bookkeeping Section (RAD-BKS) every 15th day of the month for submission to management thru RAD, för the purpose of reporting collection performance by implementing offices.

3. The interim trial balance shall consist of all collection book transactions recorded and approved as of the 15th day of the current month. This procedure shall facilitate timely and accurate reporting, recording and reconciliation of collection figures.

4. The deadline for the submission of the Year-end Pre closing and Post Closing TB, FS and SS shall be on or before March 25 of the following year for the Regional Office Collection Books (ROCB) to RAD, and March 31 for the consolidated collection books to COA.

The three (3) month deadline for the Year-end Pre-closing Trial Balance shall be deemed enough time to account for all collection data and to receive the corresponding supporting documents for the closing calendar year.

Any additional collection data and its corresponding supporting documents received and accounted for after the 31st of March shall be recorded in the collection books for the current year as prior year adjustments.\

5. The recognition, derecognition, transfer in and transfer out of collection from one collection book to another (e.g., National Office Collection Books to ROCB and/or vice versa) shall be strictly supported by} the signed and approved copy of the corresponding Journal Entry Vouchers (JEVs) from the receiving collection books within two (2) days from receipt hereof.

6. The preparation of JEV should be dated not earlier than the date of receipt of supporting documents. The only exception shall be during the preparation of the year-end Revised FS where all collection transactions for the closing year are duly accounted för and recorded in its proper collection period/calendar year.

7. The recognition of the constructive receipt of tax revenue from SARO in the NGCB shall be debited to the account Cash-Tax Remittance Advice (CTRA) instead of CTADR account.

8. Regional Collection Division (RCD) shall prepare the Summary Report of Approved Retention and Manual Transfer of collection and forward the duly signed report to RFD as basis for recording in the ROCB.

9. The Tax Receivable to be recorded in the NGCB shall be reported by RCD and the concerned Large Taxpayer Offices to their respective RFDs and RAD duly supported by proper documentation.

10. The following pertinent information on Tax Receivables shall be disclosed in the quarterly Notes to FS in compliance with IPSAS 19:

a. Bureau’s policies and procedures or guidelines on Tax Receivables;

b. Movement of Tax Receivables;

c. Aging of Tax Receivables; and

d. Level of Collectability of Tax Receivables.

11. The RCD shall prepare the quarterly Movement and Level of Collectability of Tax Receivables and forward said reports to RFD for disclosure in the Notes to FS and to ARMD for consolidation.

12. The RCD, RFD, ARMD and RAD shall prepare and submit to concerned offices the following prescribed reports:

| Office

Responsible |

Name of Report | Deadline

(After the end of the quarter) |

Receiving Office |

|---|---|---|---|

| RFD | Aging of Tax Receivable | 6th day | RCD and RAD |

| eNGAS-generated GL of the Tax Receivable account | |||

| RCD | Movement of Tax Receivable | 8th day | RFD and

ARMD |

| Level of Collectability | |||

| RAD | Consolidated Aging and GL of Tax Receivable | 8th day | ARMD |

| ARMD | Consolidated Movement and

Level of Collectability of Tax Receivable |

10th day | RAD |

13. The RFD shall maintain subsidiary ledger accounts for each recorded case of Tax Receivables in the eNGAS for monitoring purposes.

14. The policies prescribed in RMO No. 30-2021 re: Recognition of Absolutely Forfeited Properties in the National Government Books of Accounts, shall be reiterated as guidelines in the recording of Acquired Assets in the NGCB.

15. The following relevant information on Acquired Assets shall be disclosed under the Merchandise Inventory account in the Notes to FS for transparency and accountability of custodial functions of concerned Regional Offices:

a. Bureau’s policies and procedures or guidelines on Acquired Assets;

b. Total fair value, basis of fair value, restrictions in recording and total area;

c. Aging of Acquired Assets; and

d. List of Unrecognized Acquired Assets, fair value, total area and status.

III. PROCEDURES:

A. Recording of Transfer in/out of Collection between Collection Books

The RAD shall:

- Receive from the Data Warehousing and Systems Operations Division (DWSOD) tax collection data every seventh (7th) day of the following month;

- Prepare the following Summary Report of Transfer In/Out of Collections from one Revenue Region (RR) to concerned RR:

a. Summary of Validated Transfer-Out from Out-of-District Collections (Annex C of RMO NO. 56-2019), and

b. Summary of Validated Transfer-In from Out-of-District Collections (Annex D of RMO NO. 56-2019). - Send thru email to the concerned RFD and RCD the scanned copy of the Summary Report of Transfer in/out of Collections;

- Prepare Summa1Y Report of Transfer In/Out of Collections from Large Taxpayer (LT) offices to RR;

- Prepare JEV to record the transfer in/out of collections to/from the NOCB or LT Offices from/to the ROCB and send thru email to the concerned RFD the scanned copy of approved RAD JEV and supporting report;

- Receive from RFD the scanned copy of approved RFD JEV within two (2) days from receipt of email;

- Check correctness of details of approved RFD JEV, and

- Attach RFD JEV as supporting document to the corresponding RAD JEV for submission to COA.

The RFD shall:

- Receive from RAD thru email the following scanned copies: Approved RAD JEV recording the transfer in/out of collection from/to LT Offices to/from ROCB, and Summary Report of Transfer in/out of Collections from LT to RR.

- Check correctness of details of RAD JEV against the supporting report;

- Prepare and approve JEV to record the transfers in/out of collection to/from the NOCB from/to the concerned ROCB;

- Attach RAD JEV and supporting report to the RFD JEV for submission to COA; and

- Send to RAD scanned copy of approve RFD JEV within two (2) days from receipt of the following scanned documents:

a. Approved RAD JEV recording the transfer in/out of collection from/to LT Offices to/from ROCB, and

b. Summary Report of Transfer in/out of Collections from LT to RR.

B. Procedures in the Disclosure of Tax Receivables in the Quarterly Notes to FS

The RFD shall:

- Prepare the quarterly Aging of Tax Receivables;

- Export from eNGAS the quarterly General Ledger (GL) of the Tax Receivable account;

- Transmit the Aging and eNGAS-generated GL of the Tax Receivable account to RCD for reference, and to RAD for consoli4ation on/before the sixth (6th) day after the end of the quarter;

- Receive from RCD the Quarterly Movement of Tax Receivable and the Probability of Collection on/before the eight (8th) day after the end of the quarter:

- Reconcile balances in the Movement of Tax Receivable against the balance in the eNGAS-generated GL;

- Coordinate any identified discrepancy with RCD; and

- Disclose in the Notes to FS the Movement of Tak Receivable and Probability of Collection.

The RCD shall:

- Receive from RFD the Aging and eNGAS-generated quarterly GL of the Tax Receivable account for reference on/before the 6th day after the end of the quarter;

- Reconcile the balances of the Unpaid Revenue General Ledger and the eNGAS generated GL of Tax Receivable;

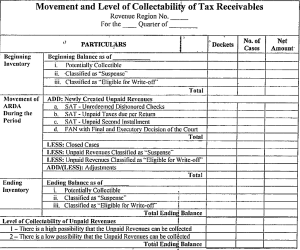

- Prepare the Quarterly Movement of Tax Receivable and the Probability of Collection using the following format:

- Submit to RFD for disclosure in the ROCB Notes to FS, and to ARMD for consolidation on/before the eight (8th) day after the end of the quarter.

The ARMD shall:

- Receive from RCD the Movement of Tax Receivable and Probability of Collection on/before the 8th day after the end of the quarter;

- Receive from RAD the Consolidated Aging and’ balance of the Tax Receivable account per ROCB on/before the 8th day after the end of the quarter;

- Check the correctness of details of both reports and reconcile;

- Consolidate all Movement of Tax Receivables and Probability of Collection from all RRs: and

- Submit to RAD the Consolidated Movement of Tax Receivable and Probability of Collection on the tenth (10th) day after the end of the quarter for disclosure in the consolidated Notes to FS of the NGCB.

The RAD shall:

- Receive from RFD the Aging and eNGAS-generated GL of the Tax Receivable account on/before the 6th day after the end of the quarter;

- Prepare the Consolidated Aging and balance of Tax Receivable account;

- Transmit to ARMD the Consolidated Aging and balance of Tax Receivable account on/before the 8th day after the end of the quarter;

- Receive from ARMD the Consolidated Movement of Tax Receivable and Probability of Collection on or before the 10th day after the end of the quarter; and

- Disclose in the NGCB Notes to FS the Consolidated Movement and Probability of Collection of Tax Receivables.

IV. REPEALING CLAUSE:

This Order repeals all existing issuances that are inconsistent herewith.

V. EFFECTIVITY:

This order shall take effect immediately.

Copy of the RMO can be accessed thru the link below.

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.